Getting a bank loan to construct a polyhouse is a structured process that demands attention to details. Here is a step-by-step process to secure bank loan for your polyhouse project.

A commercial polyhouse project costs between ₹30 Lakhs to ₹60 Lakhs depending on the field size and polyhouse technologies. Unless you have an idle investable amount in a bank account, you will need a bank loan. But here is the harsh reality: Banks reject nearly 50% of agriculture project loans.

Why? It’s not because they hate farmers. It’s because the application lacks “Financial Feasibility.”

In this guide, we decode exactly what the Bank Manager wants to see, the difference between a Term Loan and KCC, and the “Secret Checklist” to get your loan sanctioned in record time.

The Type of Loan You Need (Term Loan vs. KCC)

Do not confuse a Kisan Credit Card (KCC) limit with a Project Loan.

- KCC (Crop Loan): This is for working capital (buying seeds, fertilizers, diesel). It is a short-term limit (1 year) usually up to ₹3 Lakhs. You cannot build a structure with this.

- Agri Term Loan (ATL): This is for Capital Expenditure (CAPEX). This is what you need for polyhouse construction.

- Tenure: 5 to 9 years.

- Moratorium: 6 to 12 months (You don’t pay principal during construction/first crop).

- Interest Rate: Usually 9% to 12% p.a. (varies by bank).

FarmAtma Tip: Ask specifically for an “Agriculture Infrastructure Fund (AIF)” loan if eligible. Under AIF, you can get an interest subvention (discount) of 3% on loans up to ₹2 Crores!

How to Lower Your Interest Rate (The AIF Scheme)

Most farmers assume they have to pay the standard bank interest rate of 9% to 11%. This is incorrect. In 2026, you must take advantage of the Agriculture Infrastructure Fund (AIF).

What is AIF? It is a Central Government scheme that provides Interest Subvention (a discount on interest) for post-harvest management projects, which includes Polyhouses.

- The Benefit: The government pays 3% of your annual interest directly to the bank.

- Example: If the Bank sanctions a loan at 9%, your effective burden is only 6%.

- The Cap: Applicable for loans up to ₹2 Crores.

- The Duration: Valid for 7 years.

- Credit Guarantee: For eligible borrowers, the government also provides a credit guarantee (CGTMSE), meaning you might need less collateral.

FarmAtma Strategy

Do not rely on the Branch Manager to do this for you. They often forget or ignore the extra paperwork. You must register online on the National Agriculture Infra Financing Facility portal and generate your “Project ID” before or simultaneously with your bank loan application. Attach the AIF registration receipt to your loan file.

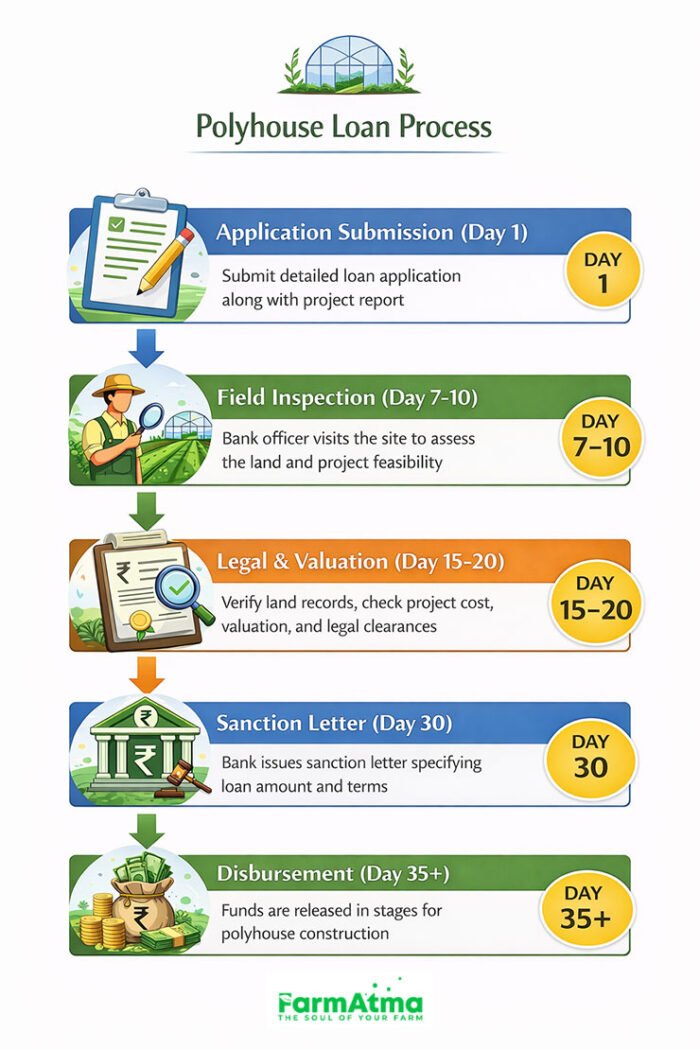

The Roadmap: From Application to Disbursement

Getting a bank loan is a step-by-step process. Do not expect the money in your account the day after you apply. In a realistic scenario, this process takes 30 to 45 days.

The 5 Stages of Sanction:

STAGE 1: Application Submission (Day 1): You submit the DPR, Land Documents, and KYC to the branch.

STAGE 2: Field Inspection (Day 7-10): The Field Officer visits your land to check if it matches the documents and if the location is suitable.

STAGE 3: Legal & Valuation (Day 15-20): The bank appoints an external lawyer (to check land history) and an engineer (to value the land). You usually pay the fees here.

STAGE 4: Sanction Letter (Day 30): If reports are positive, the Manager issues the Sanction Letter. You sign the mortgage deed.

STAGE 5: Disbursement (Day 35+): The bank does not give you cash. They release payments directly to your vendor (polyhouse constructor) in stages as the work progresses.

The Ultimate “Bank-Ready” Checklist

Don’t walk into the bank empty-handed. To get your loan sanctioned quickly, prepare these 3 sets of documents in a file.

Set A: KYC & Land (The Basics)

- 7/12 Extract (Satbara) & 8-A Extract: Current year, clear title.

- Land Map (Nakasha): Certified by the Talathi/Patwari.

- No Dues Certificate: From other local banks (to prove you aren’t a defaulter).

- Aadhaar & PAN Card: Both for the applicant (and guarantors if require).

Set B: Project Documents (The Proof)

- Detailed Project Report (DPR): Crucial. Must include cash flow projection for 7 years.

- Quotations: 3 different quotes from Polyhouse vendors (Banks require comparison to ensure pricing is fair).

- Soil & Water Testing Report: To prove the land is fertile and water pH is suitable (5.5 – 7.0).

- Permission/NOC: Gram Panchayat NOC for construction.

Set C: Collateral & Security

- Valuation Report: A government-approved valuer’s report of the land/property you are offering as security.

- Legal Search Report: A lawyer’s certificate stating the land has had no legal disputes for the last 13-30 years.

FarmAtma Tip: Ask for a “Moratorium Period” of 6-12 months. This means you don’t pay EMI until your first harvest is sold.

The Branch Manager Interview: How to Pass the Test

Submitting the file is easy. Defending it is hard. Once your documents are verified, the Branch Manager will call you for a personal interview. Their goal is to judge YOU, not the project. They want to know if you are a serious entrepreneur or just chasing a subsidy.

Here is how to answer the 5 most dangerous “Trap Questions”:

Q1: “You have no prior experience in farming. How will you manage?”

- The Trap: They think you will fail technically.

- The Wrong Answer: “I will learn from YouTube” or “Farming is in my blood.”

- The Winning Answer: “Sir, I run this as a business, not a hobby. I have already hired a Technical Agronomist (FarmAtma has a team of qualified Agronomists) who will visit the farm weekly. I have also attached a Memorandum of Understanding (MoU) with my input supplier for 24/7 technical support.”

Q2: “What if the market price crashes?”

- The Trap: They want to know if you have a financial buffer.

- The Winning Answer: “I have calculated my break-even price. My project is profitable even if I sell Capsicum at ₹30/kg. Since my production cost is only ₹18/kg, I have a large safety margin even in a bad market.”

Q3: “Why is your project cost higher than the NABARD guideline?”

- The Trap: NABARD unit costs are often outdated (old steel prices).

- The Winning Answer: “The NABARD guidelines were last updated years ago. Steel and cement prices have risen by 40% since then. My project cost is based on current 2026 vendor quotations, which I have attached to the file. I cannot build a safe structure with old rates.”

Q4: “Who will buy your harvest? Do you have an agreement?”

- The Trap: The manager knows that growing the crop is easy, but selling it is hard. If you say “I will sell in the local mandi,” you might be rejected because local mandis fluctuate wildly.

- The Winning Answer: “Sir, I am not relying on the local mandi. I have identified three specific markets: The [City Name] Wholesale Market for bulk sales, and two hotel chains for premium sales. I have also initiated talks with [Name of Exporter/Buyer] for a contract. Here is the letter of intent.”

- FarmAtma Tip: Even if you don’t have a contract, name a specific City Market (e.g., “Kolkata Mechua Market” or “Delhi Azadpur Mandi”) to show you have done your homework.

Q5: “How will you pay the EMI if the first crop fails?”

- The Trap: Banks hate lending to people who rely 100% on the project to pay the loan. They want a “Plan B.”

- The Winning Answer: “While I am confident in the project, I have a secondary source of income to service the debt during lean periods. My [Spouse/Father] earns a salary of ₹X, and we have existing income from our traditional paddy farming. We can sustain the EMI for 6 months even without polyhouse income.”

- Note: If you have IT Returns from a job or business, mention them here. It is the biggest safety net for a banker.

The “Detailed Project Report” (DPR): What Banks Look For

The Manager doesn’t read the whole book. They look at 3 numbers. Make sure your DPR highlights these:

- DSCR (Debt Service Coverage Ratio): This ratio measures if you make enough profit to pay the EMI.

- Ideal Range: > 1.5 (Means for every ₹1 of EMI, you earn ₹1.50).

- IRR (Internal Rate of Return): The percentage return on the investment.

- Ideal Range: > 20%.

- Payback Period: How fast will the bank get its money back?

- Ideal Range: 3 to 5 years.

Margin Money & Collateral: The Hard Truth

Banks don’t provide 100% financing. To mitigate credit risk, they typically require safeguards such as margin money and collateral security.

- Margin Money: You must contribute 15% to 25% of the project cost from your own pocket.

- Example: For a ₹40 Lakh project, you need to show ~₹6-10 Lakhs in your account.

- Collateral Security:

- Primary Security: The Polyhouse structure and machinery itself (Hypothecated to the bank).

- Collateral Security: You usually need to mortgage the land (or other property) equivalent to 100-150% of the loan value.

- Note: If your loan is under ₹20 Lakhs (varies by scheme), you might get coverage under CGTMSE (Credit Guarantee Fund), removing the need for collateral. Ask your banker about this!

- Hidden Costs: Don’t think the “Margin Money” (25%) is your only expense. Banks have several unwritten administrative costs that are deducted from your loan or asked for upfront. Budget for these ~₹50,000 to ₹1 Lakh expenses.

Warning: The “Funding Gap”: Government Norms vs. Market Reality

Remember, the bank will only fund based on the Government Cost Norm, not your Actual Vendor Quote. As explained in our Subsidy Guide, this creates a “Funding Gap.” You may need to arrange an extra ₹4-5 Lakhs in cash to bridge this difference. Do not rely 100% on the loan to cover construction.

Top Banks for Polyhouse Loans

While all commercial banks offer these loans, some are more “Agri-Friendly” than others.

- State Bank of India (SBI): Schemes like Multi Purpose Gold Loan or Polyhouse Scheme. Low interest rates, but strict paperwork.

- Canara Bank: Very active in South India for hi-tech farming projects. Two specific schemes are Agriculture Infrastructure Fund Scheme and Hitech Agriculture Scheme.

- Bank of Baroda: Has specific “Baroda Kisan” schemes.

- NABARD (Refinance): NABARD doesn’t give direct loans to farmers, but they refinance the banks that lend to you. Mentioning “NABARD Refinance” to your banker shows you know the system.

Why Applications Get Rejected (And How to Avoid It)

We have learned from experience that if your polyhouse loan application was rejected, it was likely due to one of these five ‘Deal Breakers.’

- Poor CIBIL Score (< 700):

- Banks are strict. If you defaulted on a credit card or a tractor loan 3 years ago or have an old unpaid bike loan, it will show up.

- Fix: Clear all old dues and wait 6 months before applying.

- Weak/ Unrealistic DSCR (Debt Service Coverage Ratio):

- This is the most technical reason. If your project shows a Net Profit of ₹5 Lakhs, but your Annual EMI is ₹4 Lakhs, your DSCR is too low (1.25). Banks generally want a DSCR of > 1.5 (meaning you earn ₹1.50 for every ₹1.00 of debt). On the other hand, if you claim you will earn ₹50 Lakhs from 1 acre in the first year, the manager knows you are lying (or naive).

- Fix: Increase the loan tenure (e.g., 7 years to 9 years) to reduce the annual EMI and be conservative.

- Land Title Issues:

- If your land is “Ancestral” and not partitioned (i.e., you don’t have a separate Parcha/Khata in your name), the bank cannot create a mortgage. If you are on leased land, the lease must be registered and cover the loan tenure (e.g., 9 years).

- Fix: Complete the land mutation process first.

- Distance from Branch:

- If your farm is 50km away from the branch, the manager cannot inspect it easily.

- Fix: Apply to a branch within a 15-20km radius of the project site. This falls under their “Service Area.”

- Lack of Market Linkage:

- The bank wants to know: “Who will you sell to?”

- Fix: Attaching a letter from a potential buyer (e.g., a local vegetable agent) strengthens your case 10x.

Conclusion: The Roadmap to Funding

Asking for a polyhouse loan is not begging; it is a business proposal. If you go prepared with your Quotations, DPR, and Collateral Papers, the bank wants to lend to you. We at FarmAtma are here to guide you step-by-step.

Your Next Steps:

STEP 1: Get Quotes: Call 3 vendors and get estimates.

STEP 2: Prepare DPR: Use our Polyhouse Cost Guide to get the right numbers.

STEP 3: Visit the Branch: Go to the “Agriculture Officer” (AO) at your local branch, not the clerk.